Deal Teams

Data-Driven Decisive Alpha

Deal teams get the tools to make data-driven investment decisions with unprecedented depth and precision. Whether evaluating a private equity opportunity, assessing a private credit deal, or analyzing a real estate investment, the platform provides comprehensive deal-level analysis that goes far beyond traditional financial models.

Outcome Probabilities

P50/P90 Return Thresholds

Value Attribution

Isolate Operational Alpha

Deal Return Scenarios

Your Excel Workflows, Augmented with Quant

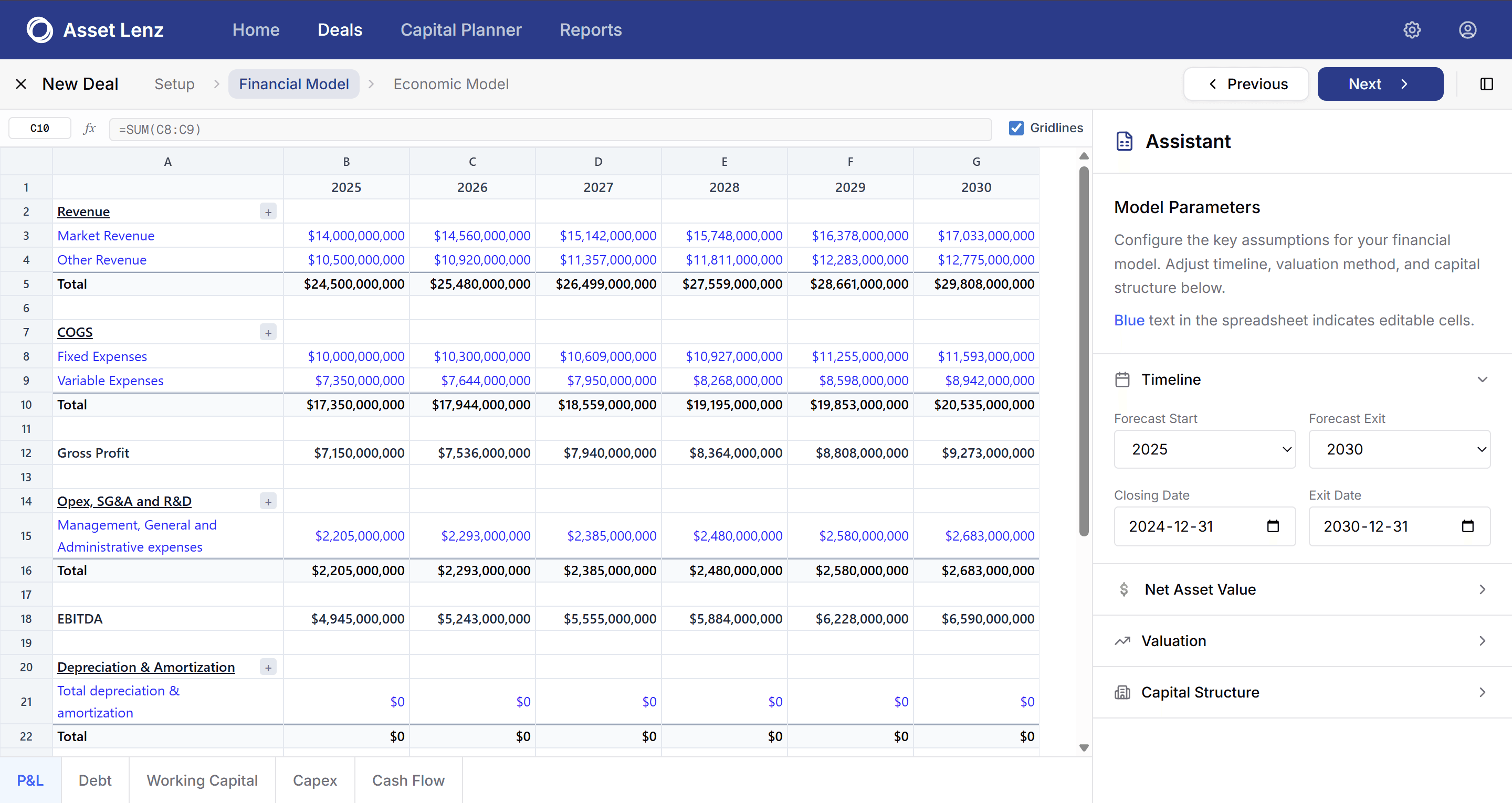

We understand that your existing Excel-based financial models are the foundation of your deal analysis. Rather than replacing them, Asset Lenz enhances your familiar spreadsheet workflows with powerful quantitative capabilities.

Our platform preserves the transparency and flexibility you rely on in Excel—with formulas, editable cells, and familiar financial statement structures—while adding structured model parameters, automated scenario analysis, and quantitative risk assessment that transforms static models into dynamic decision engines.

Maintain your firm's proprietary underwriting templates and calculation logic

Configure key assumptions through structured model parameters instead of scattered cell edits

Extend beyond single-scenario analysis with Monte Carlo simulations and probability distributions

Investor Workflow Lifecycle

Technical Ingest

Massive parsing of ARGUS broker files, messy VDR spreadsheets, and unstructured property diligence PDFs.

Our neural-extraction layers identify line items for OpEx, Rev, and Capex with 99% accuracy. We clean and structure fragmented data for immediate deterministic workbook mapping.

Quant Anchoring

Mapping revenue, opex, and debt schedules automatically to your firm's specific underwriting template.

Codify firm-specific cap-rate logic and IRR hurdle rates into a live model. Our engine builds a multi-sheet workbook with linked logic that maintains your firm's proprietary math.

Monte Carlo Risk

Apply macro shocks across 10,000+ stochastic iterations to identify P50/P90 return thresholds.

Visualize the full distribution of outcomes. Quantify tail risk (VaR 1%, VaR 5%) and Expected Shortfall (CVaR) to understand downside exposure across diverse economic regimes.

Memo Generation

Instant generation of data-backed IC memos with return bridges and sensitivity heatmaps.

Generate audit-ready briefings including value creation waterfalls (EBITDA growth, multiple expansion, debt paydown) isolated automatically for internal committee reviews.

Targeted Asset Classes

Our quant engines are fine-tuned for the unique risk drivers of every private market vertical.

Private Equity Focus

Buyout, growth equity, and control investments. We transform static Excel modeling into a dynamic probability engine for high-conviction decision making across the capital stack.

Isolate EBITDA growth from Multiple expansion alpha drivers

Monte Carlo risk distribution for IRR and MoC (5th to 95th)

Detailed Value Creation waterfalls per simulation path

Stochastic modelling of Net Debt and Working Capital dynamics

Proprietary exit-multiple sensitivity and path analysis